That leaky roof can’t wait. That 1970s kitchen is hurting your home’s value. If you’re wondering how to pay for house projects without draining your savings, you’re not alone. Using a personal loan for home improvement is an increasingly popular and smart financial strategy.

In the past, the only options were slow, complicated home equity loans (HELOCs) or high-interest credit cards. Today, a personal loan for home improvement offers a fast, flexible, and often cheaper alternative. As a financial education platform, ClearCreditLoan is here to explain why this trend makes sense and how you can use this tool responsibly. We are not a lender, but we are experts at helping you build a smart strategy to fund your project.

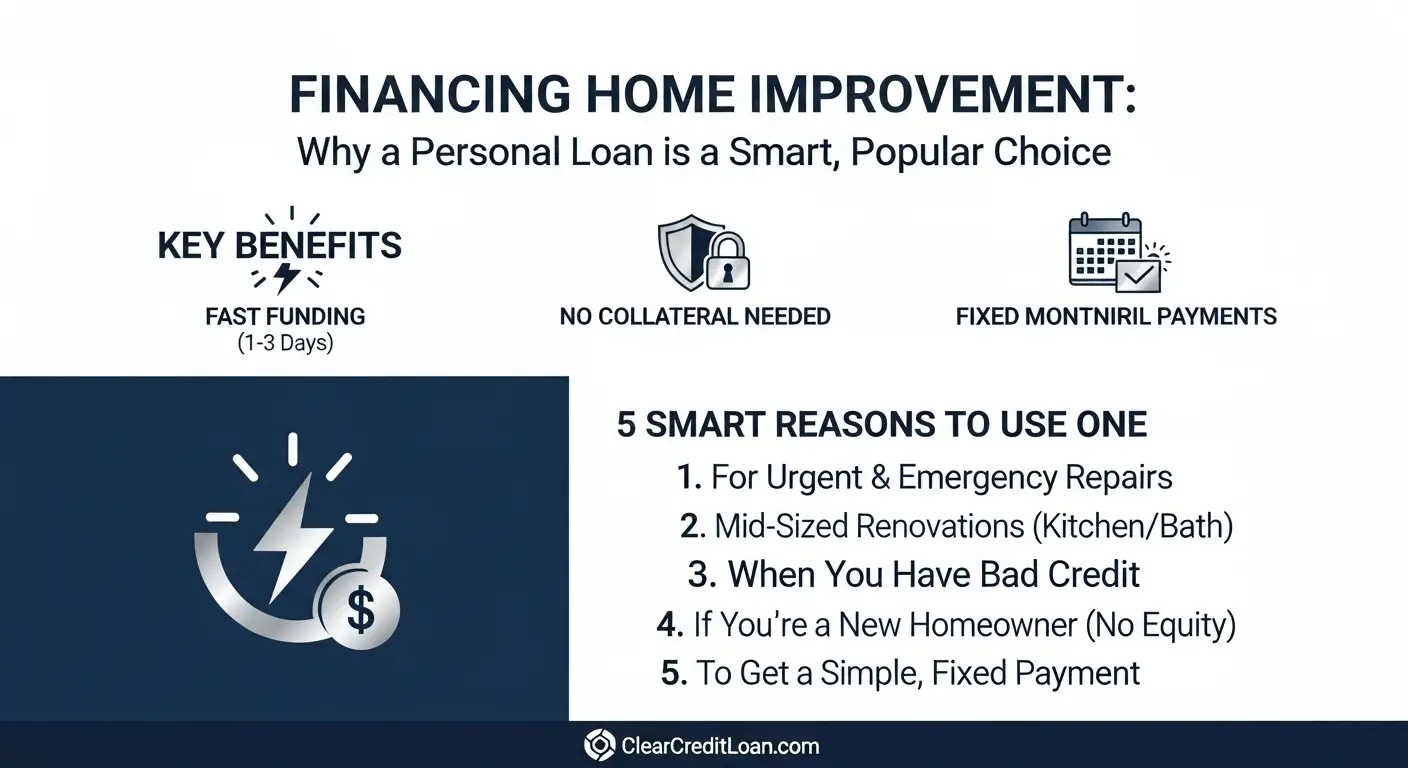

What Is a Personal Loan for Home Improvement (And Why Is It Popular)?

A personal loan for home improvement is an “unsecured” installment loan.

- Unsecured means you do not have to put your house up as collateral (unlike a HELOC).

- Installment Loan means you get a lump sum of cash upfront and pay it back in fixed monthly payments over a set term (e.g., 3-7 years).

According to the Consumer Financial Protection Bureau (CFPB), personal loans are defined by these fixed terms, which makes them much easier to budget for than a variable-rate credit card.

This combination of speed, simplicity, and no collateral is why they are becoming the go-to choice.

5 Smart Reasons to Use a Personal Loan for Home Repairs

A personal loan for home improvement isn’t just for emergencies; it’s a strategic tool.

1. Urgent & Emergency Repairs (Speed is Key)

Your air conditioner just died in July, or your water heater burst. You can’t wait 45 days for a home equity loan to close. A personal loan can often be funded in 1-3 business days. With home repair costs are rising according to CNBC, financing is often a necessity, not a choice.

2. Mid-Sized Renovations (Kitchens, Bathrooms, Decks)

For projects between $5,000 – $50,000, a personal loan is perfect. It’s ideal for a bathroom remodel or a new deck that will increase your home’s value (ROI), but isn’t large enough to justify a complex refinancing.

3. You Have Bad Credit (or Thin Credit)

This is a major reason for its popularity. It is very difficult to get a HELOC with a low credit score. However, many online lenders specialize in personal loans for various credit profiles. If you’re living with bad credit, a personal loan may be your most accessible option.

4. You’re a New Homeowner (No Equity)

To get a HELOC, you need to have “equity” (ownership) built up in your home. If you just bought your house, you have very little equity. A personal loan is based on your income and creditworthiness, not your home’s equity, making it perfect for new buyers.

5. You Want a Simple, Fixed Payment

A personal loan for home improvement is predictable. You know exactly what your payment is and exactly when it will be paid off. A credit card’s variable interest and minimum payments can keep you in debt for decades.

How to Choose the Best Personal Loan for Home Improvement

This is a smart investment, but only if you get the right terms.

- Calculate Your ROI: Will this $15,000 kitchen remodel add $25,000 in value? If yes, it’s a great investment.

- Know Your Payments: Make sure you understand how amortization works. A fixed monthly payment is easy to budget for before you borrow.

- Compare APRs (Critically Important): Do not take the first offer. Use a “soft pull” comparison tool (like our partners) to see rates from multiple lenders. The difference between an 11% APR and an 18% APR can mean thousands of dollars.

- Check for Fees: Look for low (or zero) “origination fees” and no “prepayment penalties.”

Using a personal loan for home improvement is a smart, modern financial tool to protect and grow your home’s value. But the key to a smart loan is finding the best rate.

ClearCreditLoan can help. Use our free, secure tool to compare pre-vetted loan partners for home improvement financing. See your potential offers in minutes without impacting your credit score.

{kind=link}