If you’re juggling bills and loan payments, you need a plan that protects essentials first and still shrinks your balances. This guide shows how to budget to pay off debt and cover living expenses using a simple structure, smart cuts, and automation—so progress continues even when life gets messy.

Why budgeting for debt and living costs must come together

Budgets fail when they ignore reality: rent, food, transport, insurance, and surprise costs. A successful plan links your debt strategy to your everyday cash flow, so payments are affordable, predictable, and sustainable.

The 50/30/20 starting point (and how to personalize it)

As a baseline, aim for:

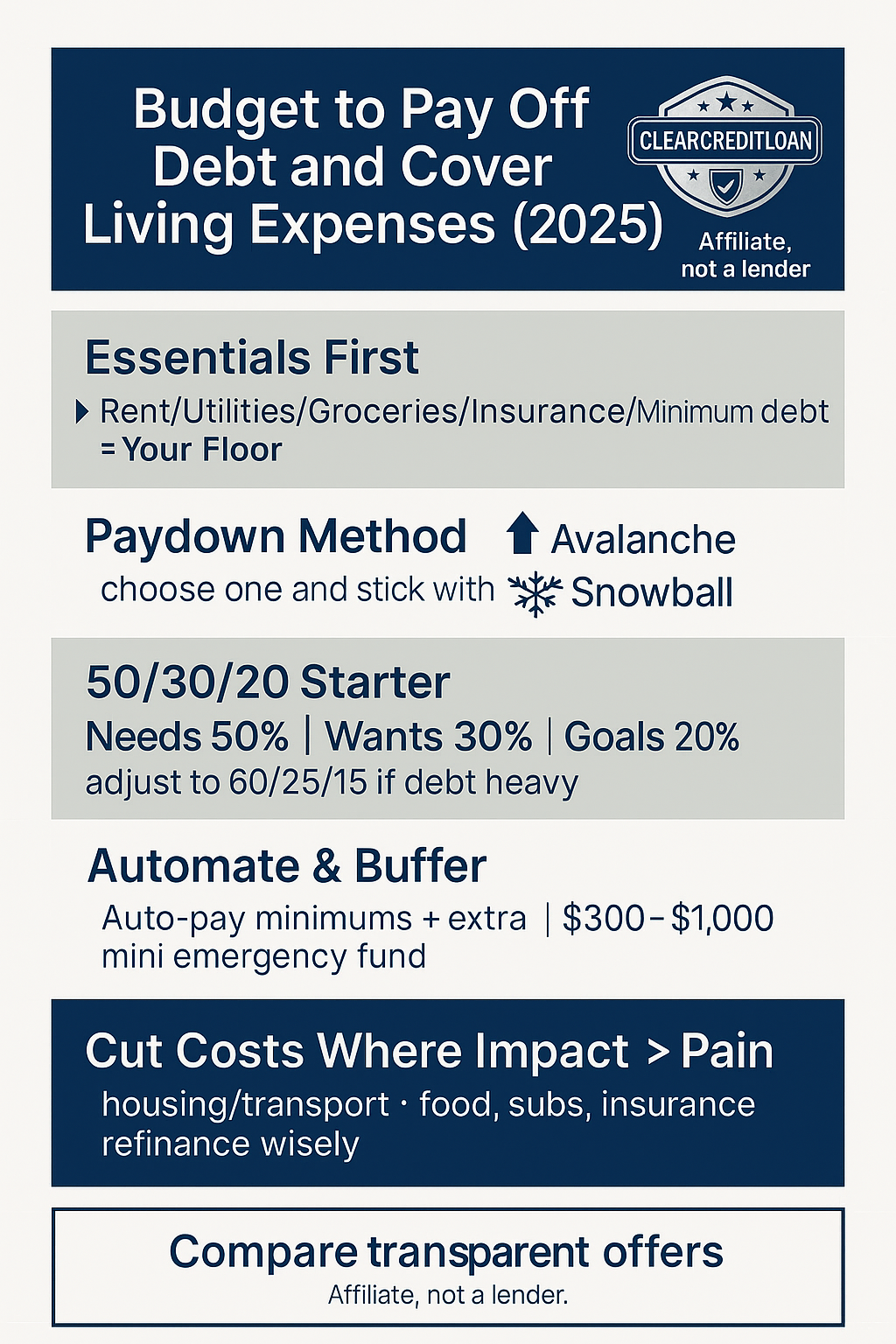

- 50% Needs (housing, utilities, groceries, transport, minimum debt payments)

- 30% Wants (nonessential spending)

- 20% Financial goals (extra debt paydown, savings)

This is a starting rule, not a law. If debts are heavy, temporarily shift to 50/20/30 (needs/savings+debt/wants) or even 60/25/15 to accelerate payoff while keeping essentials safe.

Step 1: Define your essential floor (no guesswork)

List monthly essentials with real prices: rent, utilities, groceries, insurance, transport, childcare, minimum debt payments, and any must-have medical costs. This becomes your “floor.” If income drops or expenses spike, the floor still gets paid first.

Step 2: Uncover your true APR and total cost

Know your rates, fees, and remaining terms for each loan. APR reveals the all-in cost and helps you prioritize which balances to attack first. If you need a refresher on how payment schedules work, see How Amortization Works (internal resource). For official consumer guidance on budgeting and credit, review the CFPB’s materials on money management (external resource).

Step 3: Choose your paydown method (avalanche vs snowball)

- Avalanche: pay extra toward the highest APR first for maximum interest savings.

- Snowball: pay extra toward the smallest balance first for faster wins and motivation.

Pick the method you’ll stick with. Consistency beats perfection.

Step 4: Build a mini emergency buffer

A small buffer (e.g., $300–$1,000) prevents new debt when surprises hit—flat tire, copay, appliance repair. Without a buffer, you’ll swipe a card and erase your progress.

Step 5: Automate the essentials and the extra

- Auto-pay all minimums to protect your credit and avoid late fees.

- Auto-transfer your chosen “extra” payoff amount right after payday.

- Use calendar reminders for irregular bills and annual renewals.

Step 6: Cut costs where impact > pain

Target categories that give big savings without crushing quality of life:

- Housing/transport: roommates, transit passes, renegotiate parking, telework days.

- Food: plan 10 core meals, batch cook, swap 3 takeouts/week with fast home options.

- Subscriptions: cut duplicates and “free-trial drift.”

- Insurance: re-shop annually; ask about discounts for bundling or safe-driver programs.

- Debt costs: refinance or consolidate high-APR debt only if fees are low and you will not re-borrow. See Debt Consolidation for High-Interest Loans (internal resource).

Step 7: Grow the gap (income ↑, APR ↓, time ↓)

- Side income: weekend shifts, freelancing, seasonal projects—earmark these dollars for the extra payoff lane.

- Rate reductions: ask lenders about hardship plans or interest reductions for on-time streaks.

- Term optimization: shorter terms usually reduce total interest (but raise the payment). Model scenarios before committing.

How to split each paycheck (practical template)

1) Cover the essential floor from Step 1.

2) Fund the mini emergency buffer (until it hits your target).

3) Send your fixed “extra” amount to the highest-priority debt (avalanche or snowball).

4) Allow a small, capped wants budget (or a weekly envelope) to reduce burnout.

5) If any surplus remains, split it 70/30 between extra debt and longer-term savings.

Monthly review: adjust, don’t quit

At month-end, check three numbers: (A) total spent vs plan, (B) debt balances vs last month, (C) savings buffer progress. Adjust next month’s targets. One bad week does not ruin the plan—restart immediately.

Red flags that mean “pause and reassess”

- You are borrowing to make debt payments.

- You cannot describe your APR, fees, or term for major loans.

- Your wants category keeps overrunning by 50%+.

- Your job/income is unstable and there is no emergency buffer.

Frequently asked questions about budgeting for debt

Will paying off a loan early hurt my credit? Slight score dips can happen if you close an installment account, but the interest saved usually outweighs it—especially if you keep credit utilization low elsewhere.

Should I consolidate? Only if the new APR+fees clearly reduces total cost and you lock your old cards or set strict limits.

How big should my buffer be? Start small ($300–$1,000), then grow toward 1–3 months of essential expenses once your highest-APR debt is under control.

We’re an affiliate, not a lender. Compare transparent offers by APR, fees, and term. Choose one plan that you can afford on your real budget—then automate it and protect your essentials.

{kind=link}